The CIO Monthly Perspective

DAWN OF A NEW ORDER

Cold War II and Farmageddon

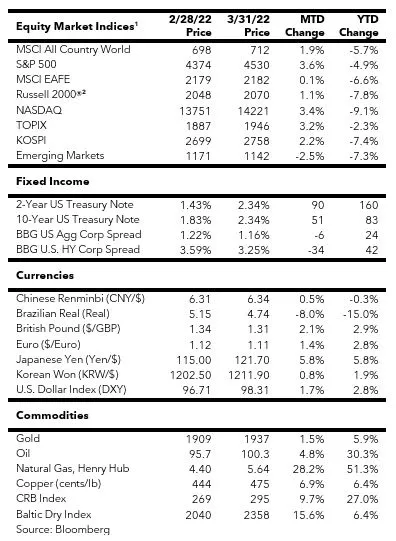

Vladimir Lenin once said, “There are decades when nothing happens and there are weeks when decades happen.” More than a century later, another Vladimir in the Kremlin proved Lenin right by launching an unprovoked attack on Ukraine, which upended the world order evolved over the last three decades. This naked aggression and the bloodiest war in Continental Europe in 77 years exacerbated the world’s inflation problem, which was already at the highest levels in forty years in the U.S. The Fed belatedly reacted to runaway inflation by commencing what may turn out to be the most aggressive tightening cycle in decades. It triggered the worst quarterly selloff in the Bloomberg U.S. Aggregate Bond Index in more than four decades and drove the U.S. 30-year fixed mortgage rate from 3.3% at the start of the year to over 4.9%.

Despite these geopolitical and economic challenges, the S&P 500 Index surging 9% and some meme stocks having more than doubled in the back half of March. Bullish investors rationalized these moves by arguing that the prior selloffs had discounted all the bad news, and that the U.S. economy, the job market, and corporate earnings have remained strong. However, historically, the fixed income market has usually been more prescient than equities, and the signals from bonds were still ones of caution. With equity valuations still at the higher end of their historical range in the face of elevated inflation and rising bond yields, the risk-reward for major equity indices do not appear to be attractive at the present time.

While many stock traders seemed oblivious of risks, officials at the White House and the State Department have been sitting on pins and needles with the highly combustible situation in Ukraine and Russia. President Biden created quite a diplomatic row in Poland when he made an off-script remark about Putin: “For God’s sake, this man cannot remain in power.” Various officials here and abroad had to quickly walk back the comment for fear of escalating tension. Well, was Putin worried about escalating tension when he invaded Ukraine? Does Putin really think that the West still wants him to stay in power? The answer is of course “NO” to both. This incident brought to mind President Reagan calling the Soviet Union an “evil empire” in 1983, for which he was roundly criticized by the liberal media and the so-called foreign policy experts. With the benefit of hindsight, that speech by Reagan is now viewed by many as a historic turning point during the Cold War. For the sake of justice and humanity, I hope Biden’s slip of the tongue turns out to be another historic and prophetic moment in the struggle between liberty and tyranny. Indeed, the eventual collapse of Putin’s regime, should it come to pass, will be a very bullish event. However, odds of a regime change are quite low in the near term as Putin will be looking over his shoulder and clinging to power for as long as possible.

THE WINTER WAR

It was a brutal war with smoldering wrecks and corpses scattered across snow-covered forests and frozen lakes in the dead of winter. The ruthless dictator in Moscow, full of hubris and bravado, thought his mighty army would easily overrun his small neighbor to the west. He did not believe this young nation of just a few decades old had any historical justification to be a real country. However, his invasion turned into a humiliating display of incompetence. There were no winners in the end, and the war was merely a prelude to even greater catastrophes to come.

Prior to the 12th century, present-day Finland was sparsely populated with three tribes – the Finns, the Tavastians, and the Karelians. In the mid-12th century, the Kingdom of Sweden started to colonize and Christianize the region. Under Swedish sovereignty, these tribes gradually developed a sense of unity and a shared identity. However, the region was frequently ravaged by wars between Sweden and Russia. In 1809, Sweden ceded the region to the Russian Empire, which made it an autonomous Grand Duchy of Finland. In 1917, the Bolsheviks overthrew the Tsar and declared a general right of self-determination for the people of Russia and the national minorities. The Finns seized the opportunity and declared independence, which was recognized by the Bolsheviks as they were still mired in the Russian civil war.

Stalin regretted letting Finland gain independence. In 1939, he signed a nonaggression pact with Germany, which gave him the greenlight to expand the Soviet Union’s sphere of influence to eastern Poland, the Baltic states, and Finland. After carving up Poland with Germany and coercing the Baltic states to accept Soviet military bases, Stalin set his sights on Finland.

In October 1939, Stalin demanded that Finland cede some territory on the Karelian Isthmus in exchange for land elsewhere. The Finns rejected the demand but made counteroffers. While they thought the negotiation was still ongoing, Russia staged a false flag operation on November 26th. A Soviet guard post near the border with Finland was shelled, and Russia used it as a pretext to invade Finland. On November 30th, the Soviet mobilized 21 divisions, or 450,000 men, to start the ground assault; its air force also bombed Helsinki, the Finnish capital. The attacks triggered international condemnation, prompting Soviet Foreign Minister Vyacheslav Molotov to claim that its air force was dropping humanitarian aid to help the starving Finnish population.

The Soviets expected a quick victory due to their overwhelming superiority with troops, tanks, and aircrafts. To their surprise, the Finns mounted stiff resistance even though they had neither tanks nor anti-tank weapons. The Finns made use of their forested terrain to destroy Soviet tanks at close range with logs, crowbars, and glass bottles filled with flammable liquids and a hand-lit fuse. The latter was pejoratively called Molotov cocktail after the Soviet foreign minister and later evolved into a symbol of resistance and riots.

As this war of attrition dragged on, Finland’s military supplies were getting exhausted while its casualties mounted. The eagerly anticipated Franco-British expedition troop was not going to arrive in time as Norway and Sweden had refused to grant it the right of passage for fear of provoking a German attack. On March 6, 1940, the Finns reluctantly proposed an armistice which led to the signing of the Moscow Peace Treaty that forced Finland to cede nine percent of its pre-war territory. Two months into the Winter War, with its numerical advantages being largely neutralized by the Finns’ resourcefulness and resiliency, the Soviet Union had not only failed to make considerable territorial advances, but also suffered mounting casualties. The bungled invasion made the country look like a paper tiger (or bear), and it was unceremoniously expelled from the League of Nations. However, as a strongman who could not afford to look weak, Stalin doubled down and sent in more reinforcements – troops were increased to 600,000, and more tanks and artillery pieces were shipped to the frontline. In early February 1940, the Red Army began relentlessly shelling Finnish positions in an attempt to bomb them into submission.

The 105-day Winter War was costly for both sides. Finland had nearly 26,000 fatalities and more than 43,000 wounded. The Soviet Union had understated its casualties officially, but historians believed that it had as many as 168,000 dead and more than 200,000 wounded. The Red Army’s poor performance convinced Hitler that he could occupy the country in a matter of months. Germany began planning an invasion of the Soviet Union just four months after the Moscow Peace Treaty was signed, and the fateful invasion – code named Operation Barbarossa – commenced on June 22, 1941. It turned out to be the bloodiest military conflict in human history. Unfortunately, in their zeal to exact revenge on and reclaim its lost territory from the Soviet Union, the Finns joined Operation Barbarossa and launched what they called the Continuation War. They had some initial success against the Soviet Union, but the war turned into a stalemate. By the autumn of 1944, Finland had to sue for peace in the face of the Red Army’s counterattack and Germany’s certain defeat. After the war, minor partner of the Axis powers, Finland had to pay reparations to the Soviet Union and swear neutrality thereafter. Foreign policy experts later coined the term “Finlandization” to characterize this forced neutrality during the Cold War.

HISTORY RHYMES

Eighty-two years after Stalin misjudged the Finns’ resolve and ability to defend their country, Vladimir Putin made a similar miscalculation about Ukraine. However, the difference this time is that Ukraine is not isolated like Finland was, as the West has finally ditched its policy of appeasement to supply Ukraine with arms to stunt Russia’s blatant aggression.

Why Putin gambled on the invasion when the threat of a war could have extracted meaningful concessions from Ukraine and the West will likely remain a mystery. His loathing of Ukrainian President Zelensky might have goaded him into the risky move. Perhaps he believed that Zelensky would flee the country and the Ukrainian military would disintegrate and surrender in the face of Russia’s overwhelming forces. He probably figured that the West would not dare to impose crippling sanctions given Europe’s dependence on Russian energy. Indeed, most investors had harbored similar views as the S&P 500 Index had surged almost 4% during the first two days of the invasion. Western leaders were initially divided on sanctions, with Italian Prime Minister Mario Draghi allegedly seeking exemptions for luxury goods exports to Russia. It drove Donald Tusk, a former president of the European Council, to tweet that everything about the war was real, but only the sanctions were pretend.

However, several days into the war, Zelensky’s Churchillian leadership, Ukraine’s spirited resistance, and rising pro-Ukraine sentiment among the electorate drove European leaders to toughen their stance against Russia. Even Hungary’s usually pro-Kremlin Prime Minister Viktor Orban has condemned the invasion and refrained from vetoing the European Union’s sanctions. Ironically, Putin has unwittingly unified the West and set in motion a major geopolitical realignment to the detriment of Russia.

DUGIN’S GRAND STRATEGY

In 1997, while Russia was still mired in economic and political crises in the aftermath of the disintegration of the Soviet Union, Aleksandr Dugin, a Russian ultranationalist and geopolitical strategist, published a seminal book, The Foundations of Geopolitics: The Geopolitical Future of Russia. The book laid out a blueprint to rebuild the Russian empire by leveraging its natural resources and various divide-and-conquer strategies to “Finlandize” Europe and isolate the U.S. Some of Dugin’s proposed initiatives include:

- Creating a “Moscow-Berlin axis” to dominate Europe and cut off the U.K., which was viewed as an extraterritorial floating base of the U.S.

- Fueling instability, separatism, and isolationism in the U.S. by kindling ethnic, social, and racial conflicts to hollow out America from within.

- Fostering a “continental Russia-Islamic alliance” built on a “Moscow-Tehran axis” to diminish U.S. influence in the Middle East.

- Annexing Ukraine, Finland, and incorporating Romania, Serbia, etc. into an “Orthodox collective East” block.

The book was so well received by Russia’s military and foreign policy establishment that it was made a textbook in the country’s most prestigious military academy, the Military Academy of the General Staff of the Armed Forces of the Russian Federation. It appears that Putin has been pursuing these initiatives over the last two decades. He has forged a close relationship with Gerhard Schröder, former German Chancellor from 1988 to 2005, and enticed German business elites to become the largest foreign investors in Russia. Russian operatives have long been known for fanning anti-European sentiment in the U.K. and political and racial tension in the U.S. via social media and other means. In the Middle East, the Moscow-Tehran axis props up the so-called Shia Crescent – the Assad regime in Syria, Hezbollah in Lebanon, and the Houthi insurgency in Yemen. Since the annexation of Crimea in 2014, Russia has been waging a proxy war with Ukraine by backing two breakaway regions.

While Putin and Dugin might have great confidence in their grand geopolitical strategy, they failed to take into account Russia’s systemic corruption, demographic time bomb, and the narrowness of their economy relative to their ambition. These problems clearly manifested themselves in the Russian military’s shockingly poor execution in Ukraine. Andrei Kozyrev, a former Minister of Foreign Affairs under President Yeltsin, attributed the Russian military’s disastrous showing to two decades of corruption that stole much of the budget earmarked for modernizing the military. The country’s low fertility rates in the 1990s and the early 2000s have led to a shrinking pool of conscripts, and those who wound up being drafted were mostly the underprivileged populace with poor morale. As such, Russia cannot afford to throw soldiers into battles with abandon as it did in prior major wars. Russia’s economy, being smaller than that of California, Texas, and New York even before the sanctions took effect, is not big enough to fund Putin’s grand ambition. In short, Putin’s colossal miscalculation might have marked the start of the eventual disintegration of his brutal regime as the West is now arming Ukrainians as a highly motivated proxy to go for Putin’s jugular. As this protracted war drains Putin’s limited resources and turns Ukraine into a graveyard for Russian soldiers, Putin’s stature in the eyes of his minions and his geopolitical leverage will only shrivel further.

PUTIN’S RUDE AWAKENING

Besides the Russian military’s poor performance, Putin was probably caught off guard by three other developments. The first surprise was how quickly his erstwhile allies in Europe turned on him. After years of condoning Putin’s bad behaviors with nominal sanctions and toothless condemnations, European leaders finally realized that Putin’s invasion of Ukraine was akin to Hitler’s annexation of the Sudetenland in 1938 and the occupation of Czechoslovakia in the following spring. Left unchecked, it will likely be only a matter of time before Russian tanks roll into other countries like Moldova, Georgia, and even a NATO member nation. Germany, having long enjoyed a unique set of privilege for years – buying Russia’s cheap energy, selling goods to China’s big market, and getting America’s military protection – probably dealt the biggest geopolitical blow to Putin’s grand strategy when Chancellor Scholz announced that the country will rearm by spending two percent of GDP on defense “from now on, every year.” Erstwhile neutral countries – Finland, Sweden, and even Switzerland – have decided to stand against Russia. The former two have seen sharply rising popular support for NATO membership, while the latter announced that it would break its long-standing neutrality to join the European Union in imposing sanctions against Russia. In one fell swoop, Putin has upended his decades long effort to cement the Moscow-Berlin axis to divide and weaken the Western alliance.

The second surprise was the West’s sanctions on the Russian Central Bank: G-7 countries have frozen Russia’s assets in their jurisdictions, which amounts to roughly 60% of Russia’s $630 billion of foreign exchange reserves. Ironically, Russia has just lost access to assets worth 2.5 times the size of Ukraine’s GDP. Impounding a sovereign nation’s assets is akin to the nuclear option in a financial war, and the U.S. has done it to only smaller rogue nations – Iran, Syria, Venezuela, and Afghanistan after the Taliban takeover. By detonating this nuclear option against Russia, the West has opened a Pandora’s box in the economic and currency realm, though the impact will likely be felt over time. In late March, the West also banned gold transactions with the Russian central bank in order to further limit its ability to support the rubles and international trade and finance.

Lastly, the private sector has taken a surprisingly strong stance against Russia. Under pressure from stakeholders and public opinion, many Western companies have begun to unwind their businesses in Russia. While Putin couldn’t care less about Starbucks and McDonald’s closing restaurants across Russia, he has to be concerned with boycotts from industrial, technology, energy, and transportation companies as they could seriously degrade the country’s military industrial and energy complexes. As a case in point, there was an unconfirmed report from the Kyiv Independent that one of Russia’s largest industrial companies, UralVagonZavod, has suspended battle tank manufacturing due to shortages of foreign sourced components. Many Western-owned tankers have stopped shipping Russian oil, which could eventually force Russia to shut off some oil wells and reduce the supply to the world market for an extended period. For once, cancel culture has been put to good use against a war criminal, but the economic uncertainty has become more elevated.

THE “END GAME” FOR UKRAINE

While the world’s attention has been focused on Zelensky’s masterful global diplomacy, the real unsung heroes have been Ukraine’s military planners and fighters who have surprised experts of all stripes by devising and executing a superb plan to dash Russia’s hope for a quick victory. Their initial success was instrumental in securing more Western military supplies, which have created a positive feedback loop. The longer they manage to stunt Russia’s military advances, the stronger Zelensky’s negotiation position becomes. With Russia having claimed to dial down its military operation near Kyiv, a complete ceasefire in the not-too-distant future has become more probable. Putin may find a face-saving way to claim “victory” before Russia’s May 9th Victory Day, which celebrates the end of their Great Patriotic War (aka WWII). In the meantime, Russia will try to seize as much territory as possible in southern and eastern Ukraine – the former would create a land corridor to Crimea and limit Ukraine’s access to the Sea of Azov and the Black Sea, the latter is rich in natural resources such as wheat and natural gas reserves. On the other hand, the war could drag on if Putin really shares Aleksandr Dugin’s belief, expressed at a recent interview, that characterized the “special operation” as a struggle between light and darkness for the unity of the East Slavs. In the unlikely worst-case scenario, should Putin again miscalculate and resort to chemical or even tactical nuclear weapons to make up for the incompetence of his conventional forces, he would destroy any face-saving off-ramps.

The prospect of a ceasefire has already generated a relief rally, so there might be a sell-the-news moment when it comes to fruition. It will likely be a long time before Russia completely pulls its troops out of the occupied territory east of the Dnieper River. Putin might try to re-create an East-West divide in Ukraine similar to Germany after WWII since most sanctions on Russia are unlikely to be lifted anyway.

Once the ceasefire appears to be firm, Ukraine will likely receive international assistance similar to the “Marshall Plan” as the West feels morally bound to help rebuild the country. Ukraine’s prime minister Denis Shmygal has estimated that $565 billion would be needed to rebuild the country. These are significant opportunities for various European construction, materials, engineering, and industrials companies, but the uncertainty lies in the timing and the sustainability of the eventual ceasefire.

A NEW COLD WAR

Regardless of how the Ukrainian crisis gets resolved, it is hard to see how the West can return to business-as-usual with Russia still ruled by Putin. Can you picture Western leaders standing next to Vlad the Mad for group photos at the next G20 meeting in Bali this October? It is highly unlikely that the West would roll back most of the sanctions against Russia in the foreseeable future. Of course, Putin will not sit by idly while the West works on destabilizing his regime. The likely outcome will be a new Cold War with three distinct geopolitical camps. One would be the Authoritarian Axis linking Russia, China, Iran, North Korea, Venezuela, and their satellite states in Central and Southeast Asia, Africa, and Latin America. On the opposite side is the Liberal Democracy Alliance comprised of the G7 countries, most of Europe, Australia, New Zealand, and other pro-Western nations. The third camp would consist of the so-called Non-Aligned nations, including India, Brazil, South Africa, and Saudi Arabia.

The new geopolitical realignment will likely reverse many benefits of globalization that we have been taking for granted during last few decades. Many Western entities have profited handsomely from trading with regimes known for human rights abuses and strategic ill intentions. The West has rationalized it by convincing itself that interdependency would induce stability and desirable changes – that they will become more like us. That gravy train will likely be derailed as geopolitical considerations get injected into international commerce; our dependency on so-called “frenemies” is really a national security vulnerability. In the new world order, the Authoritarian Axis and the Liberal Democracies will both rework their supply chains to reduce interdependency, which will likely lead to less efficiency and higher structural inflation. Each camp will also use its comparative advantages – be they commodities, technologies, or cheap labor – for geopolitical leverage. Russia’s abundance of essential resources from wheat, fertilizers, to energy will be employed to win over many non-aligned countries and even some of our allies. When push comes to shove, he may even borrow a page from North Korea’s Kim Jung-on to leverage his nuclear and hypersonic arsenals to coerce concessions from the West. In short, profound changes are unfolding before our eyes, and some of the impacts will only be felt over time. Of course, this new Cold War could also end abruptly should Putin suddenly die of legitimate or nefarious causes.

SLEEPLESS IN BEIJING

Putin’s war is an untimely distraction for Chairman Xi, who craves stability leading up to his expected coronation for a third term in late 2022. Xi’s “bromance” with Putin the pariah has created an opening for his rivals in the Chinese Communist Party (CCP). Xi is also under pressure from the West to refrain from assisting his bruised soulmate. Domestically, his zero-COVID tolerance policy has proven to be damaging to China’s economy and social fabric.

China will likely manage to strike a balance between avoiding Western sanctions and covertly supporting Russia. Xi realizes that he will become the senior partner in the bromance, and the CCP stands to reap much economic gains from Western firms’ exits from Russia. The ongoing tension in Europe may also distract the U.S. from containing the rise of China. The Biden Administration’s recent decision to lift Trump-era tariffs on some Chinese products without a reciprocal action might just be viewed by Xi as a sign of U.S. weakness.

The West’s draconian sanctions on Russia will accelerate China’s de-dollarization efforts. If China can manage to get Saudi Arabia to price its crude oil sold to China in renminbi, it may start a domino effect with other countries from which China buys commodities. These transactions will bypass the SWIFT network to run on China’s Cross-Border Interbank Payment Systems (CIPS). China will also reconsider how it manages its foreign exchange reserves as Western sovereign debts are no longer “risk-free” due to the risk of seizure. The challenge is that, apart from Western sovereign debts, there are few markets that are safe and big enough for China’s $3.3 trillion of foreign exchange reserves. However, the more international commerce gets conducted in yuan, the less foreign exchange reserves China will need to accumulate.

Xi’s timetable for forcibly taking Taiwan will likely be pushed out, but he is unlikely to give up this “sacred mission.” His obsequious generals may still boast that the People’s Liberation Army (PLA) can quickly conquer Taiwan, but he may not be ready to risk harsh Western economic sanctions. If Xi were honest with himself, he should reassess the PLA’s fighting capabilities. After all, the PLA has not been tested in a real battle since the 1979 Sino-Vietnamese War, and most Chinese generals were promoted to their posts based on loyalty to Xi rather than proven competency.

Chinese officials and elites are also weary of the West’s ability to seize their overseas assets. For years, they have been funneling abroad much of their ill-gotten gains and sending their loved ones to live in luxury in the West. These elites would sound unyieldingly hawkish and patriotic in public, but they would much prefer to enjoy the good life rather than sacrificing for their hubristic leader. As such, the threat of asset seizure might just be an effective deterrent against China going rogue. In short, the Sino-U.S. relationship will likely remain in a testy, bent-but-not-broken mode in the coming years until the balance of power shifts appreciably in favor of one side.

FARMAGEDDON

Air, water, food, and fuel are the most essential requirements for human subsistence. Putin’s war has already curtailed supplies and pushed up prices of energy and agricultural commodities. Unfortunately, in a matter of months, some parts of the world may go hungry due to disruptions in Russian and Ukrainian wheat exports – they respectively account for roughly 20% and 9% of the world’s total wheat exports. Meat prices will also be affected as wheat is used for animal feed. Elevated food prices and shortages are recipes for political instability, as food expenses eat up sizeable portions of disposable incomes in most emerging and frontier market countries.

The war has also accentuated problems in the fertilizer market, which was hit with rising costs and shortages even before the onset of the Russian invasion. Russia and Belarus together account for roughly 17% of the world’s fertilizer exports. With natural gas being the main raw material in producing nitrogen fertilizer and herbicides, the Green Markets North American Fertilizer Index has more than tripled from the start of 2021 while prices of herbicides have more than doubled. To add insult to injury, the U.S. farming equipment industry is also being hit with component shortages while many farmers cannot find sufficient labor. In short, a perfect storm appears to be brewing for the global agricultural market, and the odds of a humanitarian crisis are on the rise. As the food crisis worsens, consumers may rush to stockpile dry food and frozen meat just like they did with toilet paper at the onset of the COVID-19 pandemic. That would make the shortages feel even more acute in the short run. Putin will then blame the West for causing the food crisis and leverage Russia’s wheat for geopolitical gains in the Middle East and North Africa.

The challenge for the Fed is that there is not much it can do about inflation caused by food and energy supply problems. Monetary tightening can reduce demand at the margin, but it’s up to fiscal and regulatory policies to address the supply issues. However, having embarrassingly misjudged the scale and stickiness of inflation since mid-2021, the Fed must now tighten aggressively in order to restore its credibility. The good news for the Fed is that it might just be able to claim victory in mid-2023 for its war on inflation as food and energy prices could experience declines by this time next year if some of the supply problems get resolved. However, the bond market is warning that it could be a pyrrhic victory as the economy could become the collateral damage. Indeed, the 2-10 yield curve flattened to -0.061 on the last day of March – while a tiny degree of inversion is still insignificant, the direction is disconcerting. Based on historical pattern, a recession will likely emerge within two years after a definitive inversion is reached. While many will argue that the 2-10 yield curve is no longer a valid signal due to market distortions created by central banks, I would prefer to not bet against it. It’s also worth noting that valuations are still at the higher end of the historical range, which does not offer much potential upside for a risk-on stance at this time. In short, I would give heed to the adage, “Discretion is the better part of valor,” in the face of a hawkish Fed and elevated macro and economic uncertainty. That means a more defensive investment posture with an emphasis on quality and hedging.