The CIO Monthly Perspective

EMOTIONAL ROLLER-COASTER

Ebbing growth outlook, rising Fed put hope

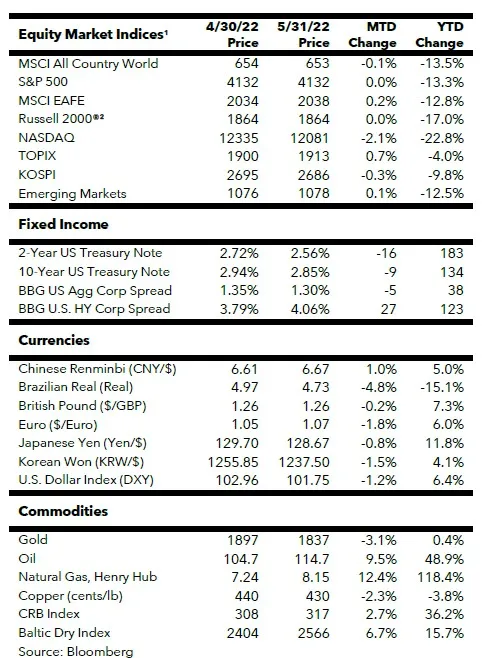

It was a roller-coaster month for financial markets as a range of investor emotions – fear and greed, hope and disillusionment – were on full display. Fears of, and disillusionment over, sticky inflation and disappointing earnings dragged the S&P 500 Index down by as much as 5.6% on a closing basis during the month, which was 18.7% below its January 3rd peak. The Index had even dipped into official bear market territory – down more than 20% from its all-time-high – intraday on May 20th when it slid to as low as 3,810. A dovish interpretation of some Fed comments then triggered investors to collectively flex their “bad news is good news” muscle memory conditioned by more than a decade of monetary largesse from the Fed; that is, economic weakness is viewed as good for stocks because the Fed will be forced to ease. The renewed optimism for the proverbial Fed put helped the S&P 500 Index storm back late in the month to finish roughly flat for May.

It has become eminently clear that higher food and fuel prices have finally taken a toll on U.S. consumer purchasing power as a long list of retailers – Walmart, Target, Dick’s Sporting Goods, Ross Stores, etc. – reported disappointing results and some even cited overstaffing and bloated inventory. While most sell-side strategists are still forecasting a soft-landing, many investors have started to discount a recessionary outcome. This increasingly cautious view has led to two positive outcomes – U.S. Treasury yields dropping like a rock over the last three weeks, and the greenback falling precipitously after hitting 19-year highs on May 12th. Falling yields and a weakening U.S. dollar are generally considered supportive to risk asset prices. The recent rally in U.S. Treasuries ended one of the worst fixed income market drawdowns in more than 40 years and raised the hope that bonds can once again act as a hedge and as a portfolio stabilizer. That said, the war on inflation is far from over as crude oil prices trended higher despite stockpile releases from the strategic petroleum reserve (SPR) and weak Chinese demand.

So far, the drawdown in the S&P 500 Index was all due to valuation contraction as the EPS estimate for 2022 has actually been nudged slightly higher since the start of the year. One can argue that equities just had a typical mid-cycle correction and that better times are ahead. However, earnings estimates will likely be the next shoe to drop since a recession or a rough economic landing appears unavoidable. Such a scenario would usually have the Fed come to the rescue with policy easing. However, with inflation unlikely to abate in a clear and convincing fashion in the near term, the much-hoped-for Fed put may be kaput for now. That said, bear market rallies can still thrive on investors’ hopes for a Fed rescue or a soft landing. Regardless of the near-term market moves, my advice continues to be staying patient, defensive, and selective.

HONOR DELAYED BUT NOT DENIED

Joseph Rochefort must have felt the weight of the entire nation on his shoulders as he paced back and forth in the cold basement office of Station HYPO, the U.S. Navy’s signals monitoring and cryptographic intelligence unit in Hawaii. It had been five months since Japan’s attack on Pearl Harbor, and he was convinced that another assault was coming in late May or early June 1942, with Midway Atoll being the most likely target. The problem was that his superiors in Washington, all the way up to Admiral Ernest King, the Commander in Chief of the U.S. Fleet, viewed him as a misfit and were ignoring his warning.

Rochefort was not a typical naval officer. He lied his way into the Navy – in 1918, he claimed he was born in 1898 rather than 1900 in order to be eligible to enlist. His penchant for solving puzzles and playing advanced card games prompted a superior to send him to a Navy cryptanalysis class. He was later trained as a code breaker. In the early 1930s, the Navy dispatched him to Tokyo to learn Japanese as the country’s militarism was on the rise. In early 1941, Rochefort was assigned to Hawaii to run Station HYPO, but his unit was denied access to the decrypts of Japan’s diplomatic messages before the Pearl Harbor attack. After the attack, he and his staff would spend long hours decoding Japanese radio messages. Sometimes he would go for days without bathing as he toiled in his office wearing a bathrobe over his uniform and walking around in slippers. By the spring of 1942, his team had broken enough code that he was certain Japan would launch an attack on a target codenamed “AF” in the Central Pacific.

Despite Washington’s dismissal, Admiral Chester Nimitz, Commander in Chief of the U.S. Pacific Fleet, trusted Rochefort’s work and asked for more intelligence. Jasper Holmes, one of Rochefort’s staff, came up with the idea of using fake intelligence to trick the Japanese navy into confirming the location of “AF”. With Nimitz’s approval, the U.S. Navy sent an unencrypted cable, knowing that it would be intercepted by the Japanese intelligence, with a fake alert that Midway had only two weeks of fresh water left due to an explosion in its water desalination system. A few hours later, the precise target of Japan’s planned invasion was confirmed as Rochefort’s team decoded Japanese naval messages instructing their armada to carry additional water desalination equipment. With the target identified, Rochefort’s team made a frenetic effort to pinpoint the date and time of the planned attack. On May 26th, they finally narrowed down the date to June 4th or 5th.

The Japanese Imperial Navy’s main objective was not the occupation of Midway Atoll. Admiral Isoroku Yamamoto’s real intention was to draw American carriers into battle and annihilate them thoroughly so that Japan could achieve naval supremacy for an extended period. Four carriers led by Admiral Nagumo were dispatched to launch the initial attacks. Another fleet commanded by Yamamoto would trail these four carriers by several hundred miles and intended to trap and overpower the U.S. fleet after the battle had gotten underway.

Admiral Nimitz had only two carriers, Enterprise and Hornet, at his disposal, but needed more to counter Japan’s larger fleet. He hastily recalled carrier Yorktown, which had suffered much damage in the Battle of the Coral Sea just a couple of weeks earlier and was undergoing repairs that would take up to three months. The crew at the Pearl Harbor Naval Shipyard somehow restored it to a battle-ready state in 72 hours.

At 4:30 am on June 4th, Nagumo ordered bombers to take off for Midway; unbeknownst to him, the U.S. Navy was also launching aircraft from Midway and the three U.S. carriers in the vicinity to search for the Japanese fleet. The bombing of Midway started at 6:20 am but failed to neutralize the heavily fortified U.S. defense. Nagumo had followed Yamamoto’s standing order to keep half of his aircraft in reserve in case any American warships were spotted. At 7:15 am, Nagumo ignored this standing order and directed these aircraft to be rearmed with land-type bombs for another raid on Midway. However, he had to reverse this order 30 minutes later upon learning that his scout planes had spotted an American carrier. His crew had to scramble to reload torpedoes onto these aircraft, which wasted precious time. In the meantime, U.S. bombers flew over and an epic battle was underway. American pilots were essentially conducting suicide missions as their planes were no match for the more agile Japanese Zero fighter aircraft. Japanese carriers repeatedly made sharp swerves to avoid bombs from above while anti-aircraft fire dotted the sky.

At 8:30 am, Nagumo had to make a tough decision: whether to immediately launch an attack on the U.S. fleet with his reserve aircraft on hand, which would deprive his aircraft returning from Midway the runway to land on the carriers and force them to dive into the sea when they ran out of fuel. He chose to forgo the immediate attack so that his forces could regroup and go after the American fleet at full strength. It turned out to be a fateful decision in the entire Pacific War.

By 10:15 am, the battle was moving in Japan’s favor as Nagumo’s four carriers had withstood waves of U.S. airstrikes with minor damage, and they were about to launch a grand scale counterattack. By chance, two squadrons of dive bombers and scout planes from Enterprise suddenly spotted the Japanese fleet. They had gotten lost and were running low on fuel, but their commander C. Wade McClusky, Jr. had decided to continue the mission. At 10:25 am, the two squadrons split up and dove down to attack Japanese carriers Kaga and Akagi. Fortuitously, the last squadron of dive bombers from Yorktown also arrived at that exact moment and went after Soryū. Defense from Japanese Zeros was ineffective as they were caught off guard and confused by these concurrent attacks from different directions. Within minutes, three of the four Japanese carriers were bombed and set ablaze. Additional explosions were triggered by parked aircraft loaded with bombs and fuel. Hiryū, the sole surviving carrier, quickly launched a counterattack by sending planes to follow the retreating American squadrons. They bombed and sank Yorktown. The celebration on Hiryū was short-lived as bombers from Enterprise and orphaned Yorktown aircraft retaliated in the late afternoon and put it out of commission with several successful hits.

As the night fell on June 4th, it was clear that the U.S. had scored a huge victory by destroying Japan’s premier battle carrier group. Nagumo boarded light cruiser Nagara and escaped westward. Yamamoto initially sent his forces eastward to continue the battle, but then retreated upon realizing that he no longer had the element of surprise or numerical advantage. By the end of the battle on June 7th, Japan had lost four carriers, a cruiser, 292 aircraft, and more than 3000 men. The U.S. lost the Yorktown, a destroyer, 145 aircraft, and 307 men.

Admiral Nimitz recommended Rochefort for a Navy Distinguished Service Medal for his invaluable contributions. However, Admiral King, still holding a grudge against Rochefort, rejected the commendation. To add insult to injury, Rochefort was reassigned to San Francisco to oversee the construction of a floating drydock just five months later. The injustice drove his former subordinate Jasper Holmes, who was duly awarded the Distinguished Service Medal, to run a multi-decade petition to award the medal to Rochefort. In 1986, ten years after Rochefort’s passing, President Ronald Reagan acknowledged that the medal was 44-years overdue and personally presented the posthumous honor to Rochefort’s children at the White House. Later that year, Rochefort was also posthumously awarded the Presidential Medal of Freedom.

LOGISTICS WINS WARS

The Battle of Midway, which was underway exactly 80 years ago, was the first major U.S. victory during World War II and marked the turning point that put Japan on the defensive. Having studied at Harvard University and served as a naval attaché in Washington, D.C., Admiral Yamamoto was keenly aware that Japan could not win a drawn-out war against the U.S. because of America’s military production capacity. Yamamoto’s sneak attacks on Pearl Harbor and Midway were intended to set the U.S. back temporarily to buy Imperial Japan time to achieve its dominance in Asia. The destruction of Admiral Nagumo’s carrier fleet had essentially sealed Japan’s and Yamamoto’s fates. He was killed ten months later during the Solomon Islands campaign – his plane was ambushed by American fighter aircraft after details of his planned trip were intercepted and decrypted by U.S. naval intelligence.

The key to America’s military might during WWII was its massive industrial production capacity. The Second War Powers Act of March 1942 allowed the U.S. government to control and allocate strategic resources and private production capacity to meet war time needs. Between 1941 and 1945, at least 64 companies had their factories seized by the government. When Admiral Yamamoto attacked Pearl Harbor and Midway, the U.S. only had 7 aircraft carriers. He would have been shocked to learn that by the end of the war, the U.S. had built 151 carriers. The U.S. military had made up for its inexperienced fighting forces, which expanded quickly from roughly 460,000 personnel in 1940 to more than 16 million by 1945 with mostly draftees, by overpowering enemies with a seemingly unlimited supply of weapons and equipment. As General John J. Pershing, commander of the American Expeditionary Forces during WWI, once said, “Infantry wins battles, logistics wins wars.”

The importance of logistics was once again demonstrated in 2022. The Russian military’s faulty logistics is one of the major contributors to its unexpectedly poor performance in Ukraine. On the other hand, the supply of increasingly more lethal weapons as well as growing financial and humanitarian aid from NATO have helped to shift the momentum of the war in Ukraine’s favor. As more NATO-supplied weapons are brought to the frontline, morale-boosting propaganda even claimed that Ukraine has been emboldened to dream of recapturing all lost territories, including Crimea. The West is now deeply involved in a proxy war with the aim of degrading the Russian military so it would be incapable of future aggression. It appears that Putin is trapped in a quagmire that he cannot extricate from unscathed.

DON’T COUNT THE BEAR OUT

While Putin’s war will likely prove to be a strategic turning point that puts the U.S. and the NATO-led liberal democracy alliance in a much stronger position versus the Moscow/Beijing authoritarian axis, there are some disconcerting developments that might complicate geopolitics, economics, and markets in the near to medium term.

The West’s solidarity against Russia has started to show a few cracks. The European Union was unable to impose a complete ban on Russian oil due to Hungary’s objection. Many European entities have succumbed to Putin’s demand that they pay for Russian gas in rubles. This maneuver has led to a sharp appreciation in the ruble, which surged to seven-year highs against the greenback before the Russian central bank intervened to weaken it. Many third-world countries have refused to condemn Putin for the attack on Ukraine, and some have increased their trade with Russia.

As the military conflict turns into a brutal war of attrition, the West’s resolve and continued support for Ukraine will be tested. Ukraine’s economy is so decimated that it will need to subsist on Western aid for years to come. As the limits of the West’s patience and aid for Ukraine get tested, there will be more pressure on President Zelensky to cede territory for peace, as suggested by Henry Kissinger at the World Economic Forum. Some so-called intellectuals in Europe have urged Western governments to stop arming Ukraine so that a compromise with Russia can be brokered. Here in the U.S., the voice of isolationism will likely get louder with the next round of funding for Ukraine; eleven GOP senators have voted against the existing $40 billion military, economic, and humanitarian aid package. If Russia can muster enough resources to drag the war into late 2022, Putin might even use the threat of cutting off natural gas to Europe during the dead of winter to weaken Germany’s support for Ukraine.

On the logistics front, the U.S. has been depleting its stockpile of Javelins and Stinger missiles. It will likely lead to reduced transfers of these badly needed weapons to Ukraine as the U.S. needs to maintain a sufficient stockpile for its own security. Our defense contractors do not have sufficient capacity to replenish the stocks of munitions needed in a protracted war. Raytheon Technologies cannot even produce Stinger missiles until 2023 due to a lack of components and materials.

In short, barring a coup or a health issue at the Kremlin, Putin still has some tricks up his sleeve to hold Europe hostage to strengthen his hand.

WOLF WARRIOR DIPLOMACY SCORES ONE

Putin’s unprovoked war and the West’s sanctions have given Beijing a free education on contingency planning for its eventual military move on Taiwan. While the West’s unprecedented sanctions against Russia may deter Chairman Xi from attacking Taiwan in the short run, he is unlikely to give up on what he considers to be a sacred mission. In recent months, the Chinese Communist Party (CCP) has started various initiatives to better shield China from potential Western sanctions.

The CCP has issued a directive prohibiting senior officials and their families from directly or indirectly holding assets overseas, which include real estate, stocks, and financial accounts. As leaks from the Panama Papers have revealed, China’s elites have transferred a massive amount of wealth overseas. Should Chinese officials really start to unload their overseas properties, it would pressure high-end real estate in metropolises from Vancouver to London. Thankfully, fire sales are unlikely as most of the properties owned by the red nobility are held indirectly via intermediaries that the Chinese call “white gloves.” The CCP also started taking steps to protect its overseas businesses from being seized by foreign governments. The China National Offshore Oil Corp (CNOOC) is reportedly working on selling its assets in the U.K. and North America.

China has taken advantage of Russia’s export bind by purchasing Russian energy in renminbi and is reportedly negotiating to buy Russian crude oil at steep discounts to fill its strategic petroleum reserve. Given China’s clout as the world’s biggest buyer of commodities, the CCP will likely pressure other countries to let it purchase commodities in renminbi, which would reduce China’s dependency on the U.S. dollar and increase the yuan’s competitiveness as a reserve currency.

The recent electoral defeat of Australia’s conservative Prime Minister Scott Morrison is probably viewed as a victory for Xi within the CCP. Morrison has incurred China’s wrath by being the first head of state to openly question the origin of the SARS-CoV-2 virus. China has retaliated by imposing tough economic sanctions against Australia to set an example for other countries. Xi would likely view Morrison’s defeat as validation of his “wolf warrior” diplomacy and be emboldened to further leverage China’s economic clout to coerce foreign politicians. With several cabinet members of Australia’s new labor government being viewed as pro-China – the Foreign Affairs Minister has pledged to repair the relationship with Beijing, and the Deputy Prime Minister’s long history of cozy dealings with China has raised eyebrows even within his own party – it will be interesting to see if China can drive a wedge in the quadrilateral security alliance among Australia, India, Japan, and the U.S., which was set up to counter the rise of China.

One issue to monitor is Australia’s policy toward the Solomon Islands, which the U.S. had liberated from Japan after the Battle of Midway at a cost of more than 10,000 American lives. Beijing has been actively courting this poor island nation of 650,000 inhabitants with generous aid as the Pacific Island region has become a key component of China’s Belt and Road Initiative. The Solomon Islands has reportedly signed a draft security cooperation agreement that would eventually enable China to establish a naval base there. If China manages to take over Taiwan and create a naval/submarine base in the South Pacific, it will be able to project its naval power across the Pacific Ocean and threaten the U.S. and its allies in East Asia as well as Oceania. The U.S. State Department was so concerned about the situation that it dispatched Assistant Secretary of State Daniel Kritenbrink to the Solomon Islands to warn that the U.S. would respond as appropriate. The U.S. also plans to re-establish its embassy there, which was closed 29 years ago, in order to counter China’s growing influence.

These developments demonstrate that the proxy war in Ukraine is merely one piece of the greater strategic rivalry between the U.S. and China. China will seize Putin’s strategic error to turn Russia into its vassal state over time. That destiny is still reversible depending on who becomes Russia’s leader in the post-Putin era, which may still be years away. At this point, it is hard to foresee a sustainable de-escalation in the strategic rivalry, or the cold war, between the U.S. and China in the foreseeable future as the latter appears determined to alter the existing rules-based international order so that it can impose its own rules. The intensity of the rivalry will also be affected by the outcome of the power struggle within the CCP as Chairman Xi maneuvers to get a third term.

AN ATYPICAL TIGHTENING CYCLE

The collapse of the Soviet Union and Deng Xiaoping’s market liberalization have paved the way for three decades of globalization, which was disinflationary and conducive to growth. Companies would scour the world for cheap labor, raw materials, and new markets. Today, with Moscow and Beijing joined at the hip in challenging the existing rules-based international order, the best days of globalization are likely behind us. This retreat from globalization, or fragmented globalization, will potentially lead to higher secular inflation as efficiency and free trade get compromised.

For now, however, investors have remained fairly complacent about the long-term inflation outlook. The 10-year breakeven inflation rate has declined to 2.67% at the end of May after briefly surging to a peak of 3.04% in April (the data series goes back to 1998). The 10-year U.S. Treasury yield has retreated from this cycle’s intraday and closing highs of 3.20% and 3.13%, respectively, to 2.84% by month end. It appears that the market’s primary concern has shifted from inflation to rapidly decelerating growth. At the end of May, the Fed funds futures market was pricing this cycle’s peak Fed funds rate at 3% by mid-2023 compared to early April’s expectation of a 3.3% peak rate by mid-2024. Atlanta Fed President Raphael Bostic floated a dovish trial balloon on May 23rd with the remark that a pause in rate hikes at the September FOMC meeting might be justified due to rapid shifts in the market that could dramatically alter outlooks. Interestingly, his comment was reinforced two days later by the release of the minutes from the last FOMC meeting, which included the sentence, “Many participants judged that expediting the removal of policy accommodation would leave the Committee well positioned later this year to assess the effects of policy firming and the extent to which economic developments warranted policy adjustments.”

These messages gave investors hope that the Fed may wrap up the tightening cycle earlier than expected. Indeed, in a typical cycle, in the face of elevated geopolitical risks, sizeable equity drawdowns, and rising recession fears, one would expect the Fed to consider shifting to neutral. This cycle, however, is anything but typical.

Historically, the Fed’s tightening cycles were anticipatory and designed to preemptively keep inflation in check. Today, the Fed is belatedly playing catchup after intentionally stoking inflation in 2020 and early 2021. Various prominent ex-Fed officials and Fed watchers have cautioned that the Fed funds rate would need to rise substantially above 4% in order to bring inflation back to the 2% target. If the Fed pauses too early due to concerns over economic growth, its already shaky inflation fighting credentials will likely be further damaged. The macro outlook could also get more complicated should Putin choose to weaponize natural gas in the winter, which would exacerbate the stagflationary shock. Another potential inflation driver is further upside in crude oil prices due to an even greater supply-demand imbalance. Since President Biden announced the historic release of 180-million barrels of crude oil from the strategic petroleum reserve in late March, the WTI crude oil price has been hitting higher highs and higher lows. This is a bullish price trend in the face of a million barrels of oil being released from the SPR each day and weak demand from a lockdown-stricken China. With more European countries starting to boycott Russian crude oil, several million barrels of Russian crude could eventually be taken off the market if Russia is forced to shut off some of its oil wells. Given the harsh operating conditions of oil wells in western Siberia, it would take years to bring production back even after sanctions and embargos are lifted.

The recent string of earnings misses from major retailers will further complicate this atypical tightening cycle as they portend a higher risk of stagflation. Which battle – economic weakness or inflation – will the Fed choose to fight? During the Great Inflation era, the Fed had raised the Fed funds rate in the midst of recession in 1974, 1980, and 1982. Chair Powell has been channeling his inner Volcker with tough talk of late, but investors do not appear to take it seriously. With three progressive-minded newcomers – Lisa Cook, Philip Jefferson, and soon-to-be confirmed Michael Barr – joining the Fed’s Board of Governors, this august body is likely to become more sympathetic to job issues than price stability

In the final analysis, I suspect the optimism for an earlier Powell Pivot is premature at this point. Fed Governor Christopher Waller tried to walk back Bostic’s dovish message by stating that he would keep 50-bps hikes on the table until there is substantial reduction in inflation. However, if the economy unravels at a much faster pace than currently projected, it is conceivable that the Fed could pause later this year. The Fed will still pay lip service to the 2% inflation target by claiming that it has successfully steered inflation in the right direction. Bond vigilantes may give it a pass due to rising recession odds, but they could drive yields to much higher levels at the other end of the recession due to higher secular inflation expectations. Over time, the Fed may elect to remove the numerical inflation target and go for qualitative goals like optimal inflation to better balance full employment and price stability. As Stephen Roach, a faculty member at Yale University, quipped recently, “I knew Paul Volcker very well, and Powell is no Paul Volcker.”

COMMODITIES AS A HEDGE

I continue to be cautious on risk assets despite the market’s renewed hope for a Powell Pivot. I suppose the pivot will happen only after the market has experienced much pain, and that the Fed will be less likely to react to drawdowns in equities than to a seizing up in the credit market. It also remains to be seen how quantitative tightening will be affected. Should the Fed wind up blinking prematurely before inflation comes under control, the road ahead may start to resemble the 1970’s environment. This argues for some exposure to commodities in one’s portfolio as a hedge.

Precious metals may rise appreciably if investors become convinced that the Fed is not really serious about tackling inflation. A stagflationary environment similar to the 1970s would be most conducive for gold and silver performance. Base metals and energy will likely be quite volatile due to cyclical drivers – they will likely pull back going into recession, and then rally with the subsequent economic recovery. They should benefit from a multi-year tailwind created by chronic underinvestment, and there are no quick fixes to supply constraints. Regulatory obstacles, geopolitical risks, and barriers created by activist investors have made it more difficult to start new mining projects. Of course, investors need to be selective on what commodities to invest in given China’s slowing secular growth potential. The urgency for many countries to fortify their energy security should favor copper, uranium, natural gas, and even crude oil and coal for a period of time. As appropriate, one could gain exposure to some of these commodities with a combination of ETFs and select mining stocks.

In the long run, owning productive assets that cannot be easily commoditized remains the best road to wealth creation. The challenge for long-term investors over the last few years was extremely elevated valuation. As the bear market has started to wash away valuation excesses, investors can selectively accumulate stocks of quality growth companies at more reasonable prices. While market drawdowns are never pleasant, they do create opportunities for upgrades and bargain hunting.

For more information on Rockefeller Capital Management: rockco.com

This paper is provided for informational purposes only and should not be construed, as investment, accounting, tax or legal advice. The views expressed by Rockefeller Global Family Office’s Chief Investment Officer are as of a particular point in time and are subject to change without notice. The views expressed may differ from or conflict with those of other divisions in Rockefeller Capital Management. The information and opinions presented herein are general in nature and have been obtained from, or are based on, sources believed by Rockefeller Capital Management to be reliable, but Rockefeller Capital Management makes no representation as to their accuracy or completeness. Actual events or results may differ materially from those reflected or contemplated herein. Although the information provided is carefully reviewed, Rockefeller Capital Management cannot be held responsible for any direct or incidental loss resulting from applying any of the information provided. References to any company or security are provided for illustrative purposes only and should not be construed as investment advice or a recommendation to purchase, sell or hold any security. Past performance is no guarantee of future results and no investment strategy can guarantee profit or protection against losses. These materials may not be reproduced or distributed without Rockefeller Capital Management’s prior written consent.

Rockefeller Capital Management is the marketing name for Rockefeller Capital Management L.P. and its affiliates. Rockefeller Financial LLC is a broker-dealer and investment adviser dually registered with the U.S. Securities and Exchange Commission (SEC). Member Financial Industry Regulatory Authority (FINRA); Securities Investor Protection Corporation (SIPC). Rockefeller & Co. LLC is a registered investment adviser with the SEC.

1 Index pricing information does not reflect dividend income, withholding taxes, commissions, or fees that would be incurred by an investor pursuing the index return.

2 Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group.