The CIO Monthly Perspective

TWIN VULNERABILITIES

Energy crisis today; chip war tomorrow

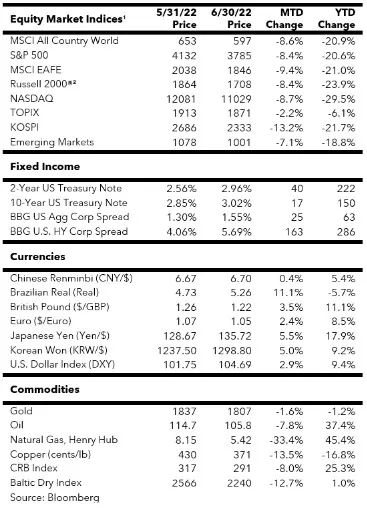

The market’s premature speculation of a dovish Fed pivot as early as this September was crushed by the harsh reality of stronger than expected inflation data released on June 10th. The data forced the Fed to hike the Fed funds rate by 75 bps at the June FOMC meeting, which Chair Powell had characterized as unlikely at his post-FOMC meeting press conference in early May. The embattled Fed Chair also pledged continued hawkishness until inflation comes down in a “clear and convincing” way. These developments dragged the S&P 500 Index into official bear market territory and triggered an epic surge in bond yields that broke the 4-decade streak of lower peak 10-year U.S. Treasury yields in successive market cycles. The 10-year yield surged to a closing high of 3.47% on June 14th (with an intraday peak at 3.49%), substantially above last cycle’s high of 3.24% reached on November 2018.

However, just when it looked as if inflation was getting out of control due to the relentless rise of crude oil prices, investors suddenly shifted their focus to the weakening economy. It may have been triggered by the realization that the Fed’s more aggressive hiking campaign will inflict sizeable damage to the economy. U.S. Treasury yields rapidly headed south with the 10-year yields falling below 3% by early July. The dramatic swings in the 2-year U.S. Treasury yield – from 2.56% at the start of June to a high of 3.43% before reversing to 2.8% at the time of writing – signaled confusion among investors about the path of the tightening cycle. Recession fears also dragged down the commodity complex from crude oil to metals. With the Bank of America’s Bull & Bear Indicator having dropped to an uber-bearish reading of zero by mid-June, traders mounted a counter-trend equity rally led by erstwhile leaders such as tech stocks. However, this much-anticipated dead cat bounce managed to gain just 6.7% and fizzled out in the last week of the month before it even got close to the S&P 500 Index’s 50-day moving average. The Index wound up losing 8.4% and 16.4% for June and the second quarter, respectively.

Undeterred, Fed officials and most sell-side talking heads have continued to push the soft-landing narrative. Wall Street analysts have also defied gravity in having revised up the 2022 earnings estimate for the S&P 500 Index since the start of the year. However, the debate among buy-side professionals who have to make real investment decisions appears to have shifted to the timing (2022 or 2023) and depth (shallow or deep) of the incoming recession. While some may argue that the market’s poor performance in the second quarter might have discounted much of the potential fundamental weakness ahead, I suspect equities have yet to test their cycle lows and would continue to advise investors to be patient, defensive, and selective.

A TRANSFORMATIONAL IMMIGRANT

Chung-Mou Chang was born into a middle-class family 91 years ago this month in the port city of Ningbo, China. While he grew up in relative comfort, his recollection of life in China was marred by war, poverty, and injustice. His family moved to Hong Kong when he was six to escape Japan’s invasion. After five idyllic years of studying at a parochial school, Hong Kong was taken over by Japan in December 1941. His family then went on a 45-day journey through multiple cities – Shanghai, Nanjing, Xian, Chengdu, etc. – to reach Chongqing, China’s wartime capital, where Chang won a merit scholarship to study at a prestigious boarding school. The family returned to Shanghai after the Sino-Japanese war but was once again forced to flee to Hong Kong in late 1948 as Mao’s Red Army swept across China.

At the suggestion of his uncle who was a professor at Northeastern University, Chang applied to Harvard in 1949 and became the only Chinese native accepted that year. 18-year-old Chang thought he was in paradise when he arrived in Boston. Freshman year at Harvard was the most scintillating time of his life, as this kid from war-torn China was suddenly exposed to a variety of stimulating experiences: classical music, opera, arts, literature, politics, basketball, and hockey. His dormmate even coached him on how to date girls. Chang also adopted a western first name – Morris.

Despite his love for Harvard, Morris realized that as a foreigner, it would be hard for him to get a good job with a liberal arts degree. In his sophomore year, he transferred to MIT where he earned his bachelor’s and master’s degrees in mechanical engineering. In 1955, he was hit with the biggest setback of his life – he had to leave MIT after twice failing the qualifying examination for a doctoral degree. He could barely eat or sleep for a week and felt deeply ashamed to face his parents and his newlywed wife. He then told himself that the show must go on and started looking for a job. Morris got four job offers and fortuitously decided to join Sylvania Semiconductor. He would spend extra hours each night reading technical papers on physics and the nascent field. Three years later, he moved to Texas Instruments (TI) as an engineering supervisor.

Under the leadership of CEO Patrick Haggerty in the 1950s, Texas Instruments was emerging as a leader in the fast-growing semiconductor industry. Haggerty spotted Morris’ talent and took him under his wing. In 1961, TI sent the 30-year-old Morris Chang to Stanford University to earn a PhD degree. Morris did not mess up this time around and received a PhD in electrical engineering in two-and-a-half years.

Upon returning to TI, Morris’ career was put on the fast track. He pioneered the practice of learning curve pricing, which automatically reduced prices on improving production yields even without customers asking for price cuts. This practice expanded TI’s market share and made it the most profitable semiconductor manufacturer of that era. Morris was eventually promoted to run TI’s entire semiconductor business.

In the 1970s, TI made an ill-conceived decision to pour resources into consumer electronics. By the late 1970s, Morris was tasked with fixing the struggling consumer group. He stayed on that job for two-and-a-half years but could not turn around a structurally bad business. He was later farmed out to a cushy staff job with a senior vice president title. Sensing that his career was at a dead end at TI, he resigned in 1983.

Morris received several job offers and joined General Instrument, a Fortune 500 company, as its President and Chief Operating Officer. It turned out to be a bad fit as his strategy of shifting the company’s growth-by-acquisition model to organic growth was met with strong internal resistance, and it led to his resignation a year later. As the suddenly unemployed 54-year-old former tech executive pondered about what to do next, a phone call came in across the Pacific Ocean.

Sun Yun-Suan, Taiwan’s former premier and one of the chief architects of the island’s economic miracle, had been wooing Morris for several years. Taiwan was attempting to upgrade its export industries from textiles, shoes, and toys to electronics and semiconductors. Morris was intrigued by the challenge and accepted an offer to be the President of Taiwan’s Industrial Technology Research Institute (ITRI), a salaried job in the public sector. A week into the new job in 1985, Morris was asked by K.T. Li, a minister tasked with developing Taiwan’s technology industry, to come up with a business plan for a semiconductor company in Taiwan within four days.

As a semiconductor industry veteran, Morris knew that Taiwan was in no position to compete head-on with the likes of Intel, TI, Motorola, and Japanese companies. He realized that Taiwan lacked talent in integrated circuit design, R&D, and sales and marketing. Taiwan’s semiconductor intellectual property, which was based on technology licensed from RCA in 1975, was about two-and-a-half generations behind the leading technology of the day. His conclusion was that Taiwan should only focus on semiconductor manufacturing, and thus the concept of a pure-play semiconductor foundry business model was born.

In 1987, Morris Chang become an entrepreneur at age 56 with the founding of Taiwan Semiconductor Manufacturing Company (TSMC). His financial backers were the Taiwanese government, Philips Electronics, and local VC firms. TSMC’s customers in the early days were vertically integrated semiconductor companies that used foundry service for older technology nodes so they could move their own fabs to more advanced nodes. Morris had also correctly predicted that TSMC’s foundry service would enable many integrated circuit (IC) designers to create their own fabless companies. Over time, as the cost of building new semiconductor fabrication facilities became prohibitively expensive, more integrated device manufacturers elected to become fabless by outsourcing their manufacturing to TSMC. It created a virtuous circle as TSMC’s economics of scale enabled it to fund more R&D to widen its technology lead over rivals. By 2017, TSMC had even surpassed Intel to become the leader in semiconductor process technology.

In 2018, Morris Chang finally retired at the ripe old age of 87. This immigrant from war-torn China has not only transformed the global semiconductor industry and Taiwan’s economy, but also created a security blanket for the island nation that has been under constant threat of attack from China since 1949. Western governments came to realize that TSMC’s semiconductor fabs in Taiwan have become a vulnerable chokepoint for the global economy: the semiconductor industry and thereby the modern economy would be taken hostage if Taiwan were occupied by China. It has elevated the West’s support for Taiwan with a greater effort in deterring China from a potential attack.

AMERICAN EXCEPTIONALISM

Morris Chang’s story is all about the American Dream, which has been shared by other immigrant entrepreneurs such as Soviet-émigré Sergey Brin, who cofounded Google, and Elon Musk, a serial entrepreneur born in South Africa. It is also about American Exceptionalism, which is founded on a set of shared values, time-tested institutions, and the generosity and ingenuity of its people. On the occasion of this great nation’s 246th birthday, we should be reminded of this exceptionalism even though some self-critical Americans dispute its existence or denigrate it as some sort of supremacy or patriarchy. If the U.S. is not so exceptional, why has it remained the world’s most desired immigration destination? Furthermore, whose leadership do other countries look to in times of international crises? Would Morris Chang, Sergey Brin, and Elon Musk have accomplished as much if they were denied an education or a business opportunity in America? Another manifestation of American Exceptionalism is that the U.S. has managed to remain a superpower despite decades of governance, or one may say mismanagement, by politicians who are mediocre at best. That said, in an increasingly competitive world with geopolitical rivals constantly working on chipping away America’s power and influence, it’s no time to rest on our laurels or to indulge in acts of self-flagellation such as revisionist histories and critical theories that dumb down our education system and diminish our institutional competence.

American Exceptionalism, especially in the spirit of innovation and entrepreneurship, has contributed to the advancement of the semiconductor industry. Semiconductors in turn played an important role in helping America win the Cold War – historian Niall Ferguson opined that the Soviet Union’s lack of access to this critical technology made it all but impossible to keep pace with the U.S. in the arms and economic races. The importance of semiconductors is not lost on China which has seen its technology crown jewel, Huawei, rapidly losing market share in the smartphone business after the U.S. cut off the company’s access to leading edge semiconductors, including the foundry service provided by TSMC. Undeterred, Huawei’s wholly owned semiconductor design house, HiSilicon, has reportedly started collaborating with Semiconductor Manufacturing International Corporation (SMIC), China’s largest foundry, to build its own fabs with older process technologies to circumvent U.S. sanctions. In other words, China still aims to be self-sufficient in semiconductor production even if it means using older technologies. It may not be able to build the most advanced chips, but its products will still be good enough for most applications, especially for military purposes.

A PRIZED STRATEGIC ASSET

It’s ironic that the world’s two most advanced semiconductor manufacturing companies, TSMC and Samsung Electronics, are located in two of the most geopolitically dangerous places – Taiwan and South Korea. While North Korea seems to enjoy saber-rattling, it is unlikely to cross the 38th parallel due to the presence of U.S. troops in South Korea. The situation in Taiwan is more complicated as most countries officially recognize it as a part of China but support its de facto independence. In recent years, China’s growing military threats against Taiwan have put a spotlight on America’s “strategic ambiguity” regarding the island nation’s security. President Trump, an isolationist, is known to have said privately that the U.S. would not defend Taiwan, but President Biden has twice said, or “misspoken,” that the U.S. military would intervene to defend Taiwan against any attack from China.

While the U.S. will likely stick to this policy of strategic ambiguity, China has made it abundantly clear that it intends to take back Taiwan. China has even raised the ante by publicly singling out the strategic value of TSMC. At a recent Chinese sponsored online China-U.S. forum with the theme of “Assessment and Response to the U.S. Competitive Strategies Against China Since the Russia-Ukraine Conflict,” the top economist of a Chinese think tank warned that TSMC is accelerating its technology transfers to the U.S. by building six plants there, and that China must not let the transfer take place. She added, “Especially in the reconstruction of the industrial chain and supply chain, we must seize TSMC, a company that belongs to China.” Coincidentally, China has been sending large sorties of bombers and fighter jets into Taiwan’s air defense identification zone after the U.S. rejected China’s recent claim that the Taiwan Strait is not international waters.

Upon realizing America’s vulnerability in its dependency on TSMC’s fabs that could be seized by the People’s Liberation Army, the Trump Administration successfully pressured the company into an agreement to construct a factory in Arizona. The agreement was inked in 2020 and the fab is expected to go into production in 2024. In June 2020, the CHIPS for America Act was introduced in the House with the goal of providing incentives to strengthen America’s global semiconductor leadership, especially in domestic production. The Senate passed its version of the CHIPS for America Act in June 2021, followed by the passage of the House version in February 2022. The final bill, which includes $52 billion of incentives, is expected to be enacted in the near future. Critics questioned the necessity of monetary subsidy since Intel has already announced in March 2021 the formation of the Intel Foundry Services. Earlier this year, Intel unveiled a $20 billion investment to build two fabs in Ohio with the production date set for late 2025. I suppose Intel’s decision to enter the foundry business and TSMC’s Arizona fab project were all predicated on some government subsidies.

IN SEARCH OF A NATIONAL INDUSTRIAL POLICY

The effort to increase America’s self-sufficiency in the critically important semiconductor industry raises the age-old question on the role of a national industrial policy. Free-market purists would argue that the U.S. government has such a poor record in resource allocation and policy execution that it should stay out of picking winners and losers. To wit, Congress has been dragging its feet on the CHIPS for America Act for two years despite its supposed criticality to national security and flip-flopping regulatory policies have cornered us into the current energy crunch. Washington’s bureaucratic incompetence has even led to the present baby formula crisis.

On the other hand, one can argue that some degree of government involvement is needed to compete against other countries’ support for strategic industries. China has hollowed out much of the West’s manufacturing capacity through decades of predatory mercantilist practices, yet it did not seem to bother free market purists as they viewed it as a natural outcome of comparative advantage. Imagine where we’d be today if our defense industry were totally left to the forces of the free market – our kids would be studying “Xi Jinping Thoughts” in American schools. In short, there has to be some middle ground when it comes to developing our nation’s strategic industries. We can let the market decide where things like shoes, handbags, and cosmetics are made around the world. However, the U.S. needs a visible hand to help protect and advance important sectors such as aerospace, advanced technologies, energy, and healthcare.

One obstacle in developing a credible national industrial policy is the public’s mistrust of the government. According to a May 2022 survey by the Pew Research Center, only two-in-ten Americans said they trust Washington to do what is right “just about always” (2%) or “most of the time” (19%). By contrast, when the survey started in 1958, 73% trusted that the government would do the right thing. The survey also showed that 65% of American adults believe that all (15%) or most politicians (50%) run for office to serve their own personal interests. Still, clear majorities of Americans believe that the government should have a major role in 11 of the 12 issue domains such as strengthening the economy, maintaining infrastructure, and keeping the country safe. It’s a sad state that most of us look to the government to solve so many issues, yet we keep on electing politicians we have so little trust in.

One encouraging development at the grassroots level is that many Americans are starting to take their children’s education into their own hands. The failings of our public education system have been known for years – over two-thirds of 8th grade students are not proficient in any core subject, according to the U.S. Department of Education’s National Assessment of Educational Progress. Lately, many parents have become further alarmed by revisionist history and “woke” curriculum that may make kids question their own self-worth and identity. As more parents voice their concerns about education at voting booths, perhaps they can help elect politicians who embrace more sensible, middle-of-the-road policies.

SKILLS MISMATCH

At a forum held by the Brookings Institution in April, Morris Chang warned that America’s plan to scale up domestic semiconductor production will be an “exercise in futility.” The problem, according to Chang, is that the U.S. does not have sufficient talent for manufacturing. Chang observed that, since the 1980s, many STEM graduates have gone into higher paying jobs in management consulting and finance rather than into industrial companies. Chang acknowledged that TSMC’s Arizona investment was a result of arm-twisting by the U.S. government, and that the cost of doing business in America is 50% higher than in Taiwan. He mentioned that TSMC’s fab in Camas, Washington has been in operation for 25 years and still trails the profitability of Taiwan-based fabs. In short, despite the risk of an attack from China, most of TSMC’s new factories will still be built in Taiwan.

It will be interesting to see how Intel, faced with similar talent shortages and cost challenges as TSMC’s Arizona fab, will manage to compete effectively in the foundry business. While Intel will receive many contracts from the Pentagon, the company may not be as competitive with commercial accounts. The construction of all these new fabs also raises the risk of overcapacity a few years from now, which could put downward margin pressure on all the players.

On the geopolitical front, TSMC’s continued buildout of its most advanced fabs in Taiwan means that the U.S. and its allies will have to defend the island nation against any attacks from China. The cross-strait tension is likely to rise further in the lead-up to the 2024 Taiwanese presidential election. The incumbent Democratic Progressive Party is known for ginning up its electoral base with the promise of Taiwan’s independence, and China will ratchet up its saber-rattling both preemptively and as a response. It will be interesting to watch how far each side will go before one of them blinks. The U.S. policy of strategic ambiguity will likely be put to the test.

THE STRUCTURAL ENERGY CRISIS

After a string of embarrassing setbacks in the early phase of the war against Ukraine, Russia appears to have gained an upper hand as of late. It has created a land corridor to Crimea, and its force has been making slow but incremental gains in Eastern Ukraine. While Western sanctions have made life more difficult for ordinary Russians, Putin’s regime is swimming in windfall profits from elevated energy and commodity prices. Russia appears to be winning the economic war for now, as much of the world has been hit by soaring inflation and rising popular discontent. Russia is expected to further reduce natural gas supply to Europe, especially during the coming winter, to break the West’s unity and to strengthen Putin’s negotiation position. The shifting momentum has emboldened Putin to proclaim the end of “the era of the unipolar world” in a defiant speech at the recent St. Petersburg International Economic Forum. He has also compared himself to Peter the Great in justifying his heinous aggression.

Faced with a prolonged energy crunch and further natural gas supply cuts from Russia, many governments have begrudgingly put aside climate concerns in favor of more practical measures. Germany is restarting coal-fired plants while Poland has lifted a ban on burning coal and wood – the government is reminding Poles to rummage forests for firewood. Here in the U.S., the Biden Administration is caught in a no-win situation as his effort to goad oil companies to increase drilling and refining has been met with derision from the right and a sense of betrayal on the left.

The energy crunch has predictably driven politicians to play the blame game and oil companies are predictably their favorite piñatas. Energy companies are accused of price gouging by deliberately holding back oil drilling and refining. Democrats are calling for windfall profit taxes to fund gas rebate cards for consumers. Senator Sanders has even introduced the Ending Corporate Greed Act, which would impose a 95% tax on excess earnings – that is, profits in excess of a company’s average profit level from 2015 to 2019, adjusted for inflation. Hmmm, shouldn’t this bill be The Government Greed Act? Unfortunately, actually resolving the energy crisis is much harder than vilifying businesses. While the U.S. is endowed with the potential to be energy independent, our domestic energy production has been hamstrung by a number of factors:

- The inconsistent nature of our energy policy, which changes with each new administration, discourages investment in long-term projects. President Biden has campaigned and made good on banning new oil and gas permits on public lands, but then reversed the policy in April in the face of elevated energy prices. The Administration then shifted to the left again by restoring authority to states and tribes to veto energy infrastructure projects such as pipelines.

- Similar to other industries, energy companies also struggle with a shortage of qualified workers. It is especially challenging to hire people willing to get their hands dirty in the harsh environment of oil fields, and younger people probably don’t want to build a career in a sector that is supposedly evil and has a dark future.

- In recent years, energy companies have yielded to investor demands to return cash to shareholders rather than funding new projects. ESG activists were especially effective in convincing investors, regulators, and even corporate executives that fossil fuel companies will face several trillion dollars of stranded assets in the future.

- Many financial services companies have been pressured by investors and regulators to scale back financing to the fossil fuel industry. Many have self-imposed caps on how much they can lend to the fossil fuel sector.

- COVID-19 induced gasoline demand destruction in 2020 has led to nearly one million barrels per day of oil refining capacity being shuttered. Some are being converted to refine renewable fuels, while others were mothballed due to loss making.

In the final analysis, there are no quick solutions to resolve the energy crunch. In the near term, it will likely take recession-induced demand destruction to help contain energy prices – the most extreme precedent had the WTI crude oil price falling from $145 per barrel to $34 in a span of five months during the Great Financial Crisis. However, the supply of crude oil is much tighter relative to demand in the current cycle. With investors having quickly shifted their main concern from inflation to recession, WTI crude oil price has dropped from June’s intra-month high of $122 to $106 at month end. With energy having been the best performing sector year-to-date, there will likely be more profit taking in the face of a looming recession. The potential drawdown among oil majors should be cushioned by their still hefty dividend yields, but E&P stocks could experience higher price swings. As investors look past the next recession, the energy sector will likely remain one of the market leaders as structural supply issues are likely to linger for years.

IN SEARCH OF SENSIBLE POLICIES

In May 1453, while the city of Constantinople was besieged by the Ottoman Turks and just a few days before its eventual fall to the Muslim invaders, the Byzantine Empire’s political, intellectual, and religious elites were still engaged in spirited debates over the sex of angels – were they male or female? To borrow a quote from Yogi Berra, it feels like déjà vu all over again as our various institutions – from education to the military – are seemingly embroiled in policy debates over pronouns, safe spaces, and the social construct of genders while our economy and national security are being threatened from within and without. Many politicians seem more motivated by winning the news cycle and rousing up their base than pursuing sensible policies that actually solve real life problems. For now, the only credible policy tool is the Fed’s tightening, which will temporarily lower demand via recession. The Administration has sought to jawbone energy prices lower by refusing to rule out the dangerous idea of banning U.S. exports of oil and refined products. An export ban can indeed crush domestic energy prices ahead of the mid-term elections, but it would severely damage our allies and U.S. leadership on the global stage, something that Putin and Xi are only too happy to see.

In the short run, the energy crisis will remain a source of instability for the global economy and financial markets. Longer term, however, the need to ensure national energy security here and abroad should create attractive investment opportunities on multiple fronts – nuclear, renewable, oil and gas, pipelines, and power grids. However, one of the biggest obstacles to upgrading our energy and manufacturing infrastructure remains the shortage of qualified workers. This is especially true in the post-pandemic era as young people would much prefer jobs that allow them to work from home over positions that require donning bunny suits in a semiconductor clean room. Ironically, the recent implosion among tech startups, bursting of the crypto bubbles, and potential job losses of the next recession just may alleviate the labor shortage and make manufacturing and oil field jobs more palatable to once-choosy workers. In the long run, the U.S. may need something akin to a national workforce policy to ensure the viability of our economy and national security. We need to fix our dysfunctional education system, contain the runaway cost of college education, and consider a merit-based immigration system as well as programs similar to Germany’s apprenticeship model. Let me wrap up this report with some green shoots on the education front: San Francisco’s prestigious Lowell High School will return to merit-based admissions, and MIT has reinstated the SAT/ACT requirement for applicants as math aptitude is important for STEM after all. In short, don’t bet against American Exceptionalism.

For more information on Rockefeller Capital Management: rockco.com

This paper is provided for informational purposes only and should not be construed, as investment, accounting, tax or legal advice. The views expressed by Rockefeller Global Family Office’s Chief Investment Officer are as of a particular point in time and are subject to change without notice. The views expressed may differ from or conflict with those of other divisions in Rockefeller Capital Management. The information and opinions presented herein are general in nature and have been obtained from, or are based on, sources believed by Rockefeller Capital Management to be reliable, but Rockefeller Capital Management makes no representation as to their accuracy or completeness. Actual events or results may differ materially from those reflected or contemplated herein. Although the information provided is carefully reviewed, Rockefeller Capital Management cannot be held responsible for any direct or incidental loss resulting from applying any of the information provided. References to any company or security are provided for illustrative purposes only and should not be construed as investment advice or a recommendation to purchase, sell or hold any security. Past performance is no guarantee of future results and no investment strategy can guarantee profit or protection against losses. These materials may not be reproduced or distributed without Rockefeller Capital Management’s prior written consent.

Rockefeller Capital Management is the marketing name for Rockefeller Capital Management L.P. and its affiliates. Rockefeller Financial LLC is a broker-dealer and investment adviser dually registered with the U.S. Securities and Exchange Commission (SEC). Member Financial Industry Regulatory Authority (FINRA); Securities Investor Protection Corporation (SIPC). Rockefeller & Co. LLC is a registered investment adviser with the SEC.

1 Index pricing information does not reflect dividend income, withholding taxes, commissions, or fees that would be incurred by an investor pursuing the index return.

2 Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group.